On August 24, 2023, during the sidelines of the 15th BRICS summit in Johannesburg, the coalition of five emerging countries spearheaded by the host President Cyril Ramaphosa approved the admission of Saudi Arabia, Egypt, Iran, Ethiopia, Argentina, and the United Arab Emirates as full time members starting January 1, 2024, bringing the total number of members to eleven in a single swift move. These new members are united by their shared position as oil-rich countries.

Would the new BRICS+ arrangement enable BRICS to finally realise its exalted goal of shifting the centre of gravity (of power) to the east?

Currently, the BRICS region is home to around 40% of the world's population, accounts for a quarter of global GDP, and occupies roughly a third of planet's total land area (BRICS India, 2021). Unfortunately, the bloc frequently finds itself under fire for its members' divergent foreign policy objectives. Despite having established its own financial institution, the New Development Bank (NDB) in 2014, the BRICS have not been able to create a meaningful impact on global geopolitics.

Jim O'Neill, an economist at Goldman Sachs, proposed the concept of a new world order in 2001, involving a coalition of emerging and developing nations lined up to transform the global economic landscape by 2050. As a consequence, thisinformal groupof four nations came into being in 2009 on the pusuance of Russia, and South Africa later joined in the same year. BRICS remains virtually inert fourteen years later. Where exactly did things go awry?

It is crucial to keep in mind that the participation of China and India together in any alliance, whether it the SCO or BRICS, typically leads in the group being neutralised due to the inherent tensions and divergent opinions of these two large countries on a number of matters (Smith, 2023).

The Shanghai Five, which later developed into the SCO, was established with the objectives of mutual security, political collaboration, and economic cooperation. The significant turning moments that revealed the group's callousness and ineffectiveness were its refusal to address India's geostrategic worries about Pakistan and the escalating unrest in Afghanistan (an SCO observer country) after the Taliban's ascent to power in 2021.

Coming back to our fundamental issue, let us examine the BRICS' efforts to oppose the dominance of the US currency:

Setting up of the New Development Bank (NDB) and the Contingent Reserve Arrangement (CRA);

The NDB's pledge to use local currency for funding rather than merely the US dollar;

Lastly, setting up of a unified BRICS Pay system for retail transactions across member countries.

At the sub-BRICS level, too, there have also been several initiatives towards the de-dollarization trend. For instance, in 2015, roughly 90 percent of bilateral trade between China and Russia was carried out in US dollars; by 2020, the percentage had dropped to 46% (Simes, 2020). In addition, China and Russia have started operating their own cross-border payment networks in tandem with the US-run SWIFT network (the Society for Worldwide Interbank Financial Telecommunication).

Dethroning of a dominant currency- déjà vu?

Historically, the establishment of a dominant currency and the transition from one dominant currency to another did not come as a result of unilateral or collective efforts of the states.

The death of Dutch gilder as a dominant currency in Europe and simultaneous rise of British Pound was not a product of Bank of England’s efforts, rather, it was due to gradual loss of confidence in Bank of Amsterdam’s failure to contain the stability of economy (refer to my previous article on Tulip-Mania).

Similarly, the Bretton Woods Conference formally recognized the US dollar’s global reserve currency status, without the US government imposing this status on other states (Eichengreen and Flandreau, 2008).

The Japanese government’s attempt to internationalize the Yen through multiple mechanisms, such as establishing an offshore market and increasing Japan’s foreign aid using the yen, failed due to Japan’s economic and social stagnation (ageing population) since the 1990s (Wu & Wu, 2014).

Can BRICS truly de-dollarize the US-led global financial system?

De-dollarization efforts by BRICS have broad ramifications for both intra-BRICS financial interactions and global financial dynamics. To exert economic power and enforce sanctions on its enemies, the US depends upon the dollar's hegemony. De-dollarization would reduce the US's ability to sway the actions of its rivals, paving the way for a more 'fair' and open order.

All five BRICS nations have historically been subject to US sanctions, with China and Russia presently facing penalties at various degrees. Some academics contend that the 2007–2008 global financial crisis and the world's economic imbalances were mostly caused by the absence of alternative institutionalised currency coordination.

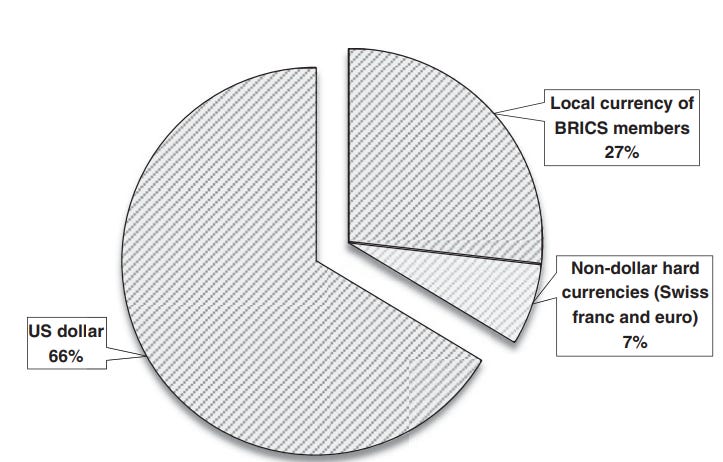

NDB Cumulative loan approvals by type of currency, as of Dec 31, 2019 (Source: NDB Annual Report, 2019)

The BRICS nations have two options for accomplishing de-dollarization: "Go it alone" and "Reform the status quo" (Liu & Papa, 2022).

"Go-it-alone" tactics entail creating fresh, non-dollar-based organisations or market mechanisms in order to diversify currency risks and keep open market access.

"Reform-the-status-quo" advocates renegotiating the terms of the current system and weakening the US dollar's predominance by engaging in collective bargaining with other countries.

Both tactics are being used by BRICS members, although they are not very successful. The figure above shows how more than half of NDB’s lending operations (~66%) are still carried out in US Dollar.

Although each of the BRICS nations has implemented a number of steps to lessen its reliance on the dollar, no economies of scale have yet been achieved. For instance, India maintains Special Vostro Rupee Accounts with 18 trading partners, including Singapore, Sri Lanka, Iran, the United Arab Emirates, Japan, and a few African countries. China has constructed cross-border communication networks and launched the yuan oil futures contract.

What are some Trade-offs?

Dedollarization poses a risk to the foreign reserves of BRICS nations like South Africa and India since they possess sizable US dollar reserves.

Certain BRICS members have stronger relations to the United States than to other BRICS countries. This is clear from India's ties with China and the US.

Finally, there is no group-level agreement among BRICS members on de-dollarization, and not all share the same urgency to lessen reliance on the US dollar while staying linked into the US-led global financial system.

Even Russia, which is pushing dedollarization forward vigorously, is not doing it on purpose. President Putin during a presser— "Russia did not want to give up the dollar as a reserve currency or a means of payment, but it was forced to do so" (TASS Russian News Agency, 2021b).

Due to their political, economic, and ideological diversity, the BRICS are unable to significantly alter the current system (Radulescu et al., 2014; Tierney, 2014; Li, 2019). The group's failed attempt to establish its own credit rating agency, which is critical for New Development Bank lending operations, demonstrates its limited ability to influence the global financial system (Helleiner and Wang, 2018).

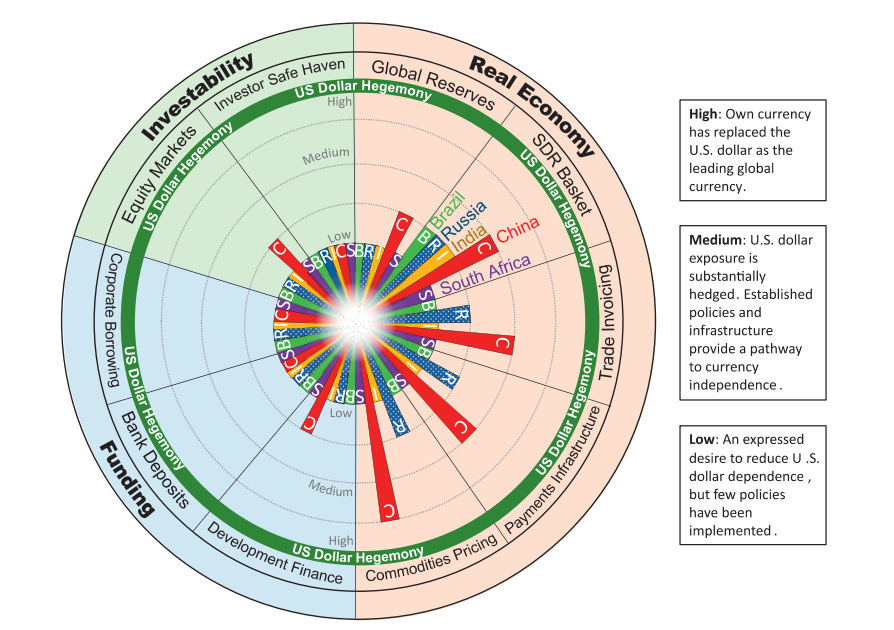

The most immediate approach for the BRICS to reduce their reliance on the US dollar is to increase their use of their national currencies in cross-border business. The Chinese yuan (Renminbi) is now the most widely traded emerging market currency, with the Indian rupee ranking second among BRICS currencies and 16th worldwide, accounting for around 1.7% of global commerce. BRICS has a long way to go in reforming the global financial landscape, and its ability to disrupt the status quo remains restricted for the time being.

—x—

By the way, did you know that Afghan Embassy has ceased its operations in India wef October 1, 2023? Read here